MoatLane.com

Anand Rawani, CFA

EPL Limited | BSE: 500135 // NSE: EPL

From a capital allocation perspective, EPL offers a combination of steady earnings growth, resilient operating cash flows, and reinvestment capability. The current valuation provides a margin of safety relative to the company’s historical trading range.

- EPL is a global manufacturer of multilayer packaging tubes with 20 manufacturing plants across 10 countries, producing over 9 billion units annually. Sales are primarily conducted through direct B2B engagements with global and regional brands under long-term repeat supply relationships.

- Clientele includes large multinational consumer goods companies such as Colgate-Palmolive, Procter & Gamble, and Unilever. ~50% of revenue is contracted. Customer concentration remains a key risk.

- Revenue growth has been steady at 7-9% CAGR. Product mix is improving toward higher-margin Personal Care and Pharma segments, now comprised 48% of revenue and growing faster than the core Oral Care segment.

- Sustained growth in profitability, with EBITDA margins recovering to ~20%. However, margins remain exposed to polymer price volatility and input cost cycles.

- Cash flow generation is structurally sound (CFO ~80–85% of EBITDA) but free cash flow remains volatile due to high and recurring capex requirements.

- The announced merger with Indovida (Indorama Group) is strategically relevant, creating a larger, integrated packaging platform with pro forma revenue of ~INR 84 bn and EBITDA margin of ~21%, with identified synergies.

- At current valuation levels (~8.2x EV/LTM EBITDA multiple), EPL trades below both recent private-market transaction benchmarks and its own long-term trading valuation averages.

Get Access to Stock Ideas

Each idea reflects our commitment

to long-term ownership

Want More Details? Write to us at arawani@moatlane.com

- On 29 March 2026, the board of EPL approved the merger of Indovida India Private Limited, a wholly owned subsidiary of Indorama Ventures, into EPL through an all-share transaction. Indorama will receive 286 EPL shares for every 10,000 Indovida shares, resulting in a 51.8% ownership in EPL post-merger. Blackstone Inc.’s stake is expected to dilute from ~26% as of March 2026 to ~16.6%.

- Based on the transaction terms, Indovida is valued at an equity value of INR 62.6 bn and an enterprise value of INR 60.9 bn (7.5x LTM EBITDA of INR 8.1 bn as of 12/2025). EPL is valued at an equity value of INR 110.2 bn and an enterprise value of INR 116.2 bn (12.4x LTM EBITDA of INR 9.3 bn as of 12/2025). In comparison:

-

- Blackstone had acquired a majority stake in EPL in April 2019 at an implied valuation of ~9x EV/EBITDA.

-

- On April 22, 2019, Blackstone announced that they entered into a definitive agreement with Ashok Goel Trust to purchase a majority stake (51%) in Essel Propack Limited (EPL), at INR 134 per share. The open offer price was fixed at INR 139.19 per share.

-

- Indorama Netherlands B.V. acquired a significant minority stake (24.9%) in EPL in February 2025 at an implied valuation of ~10x EV/EBITDA.

-

- On February 24, 2025, Blackstone entered into a definitive agreement with Indorama Netherlands, B.V., a group entity of Indorama Ventures Public Company Limited. INBV acquired a minority stake of ~24.9% of EPL from Blackstone at a purchase price of INR 240 per share.

-

- Blackstone had acquired a majority stake in EPL in April 2019 at an implied valuation of ~9x EV/EBITDA.

-

- On a pro forma basis, the combined entity would have generated LTM revenue of INR 83.8 bn and EBITDA of INR 17.5 bn (20.9% EBITDA margin) as of December 2025.

- The stated strategic rationale includes integration of flexible and rigid packaging capabilities, expansion in emerging markets, and cross-selling and cost efficiencies, with identified synergies of USD 35–50 million across revenue and costs.

- The transaction is subject to regulatory and shareholder approvals and is expected to close by the end of FY2027.

Get Access to AR FlexiCap Model Portfolio

A curated equity model portfolio designed for long-term investors

Want More Details? Write to us at arawani@moatlane.com

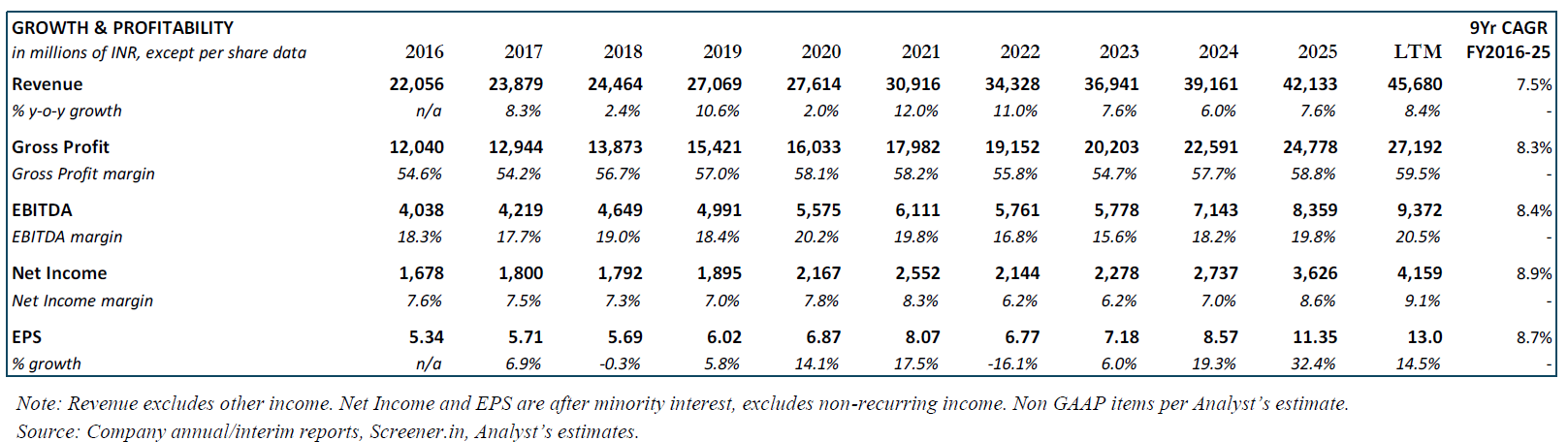

EPL, headquartered in Mumbai, India, manufactures and sells multilayer collapsible tubes and laminates used for packaging consumer products in sectors such as Oral Care, Beauty & Cosmetics, Pharmaceuticals, Food, and Home Care. The company operates 20 manufacturing facilities across 10 countries, producing over 9 billion tubes annually. Tubes manufactured by EPL incorporate up to 35% post-consumer recycled (PCR) content, reducing their reliance on virgin plastic. About 33% of packaging is recyclable. Sales are primarily conducted through direct B2B engagements with global and regional brands under long-term repeat supply relationships. Sales are supported by local manufacturing and distribution in key markets including AMESA (Africa, Middle East & South Asia), East Asia Pacific (EAP), Europe, and the Americas. Clientele includes large multinational consumer goods companies such as Colgate-Palmolive, Procter & Gamble, and Unilever, alongside regional and local brands. Customer relationships are typically long-standing. A meaningful share of revenues is derived from key accounts. Oral Care remains the largest segment, while non-oral categories such as Beauty & Cosmetics and Pharma form a growing share of revenues. In FY2025, EPL reported revenue of ~INR 42 bn and EBITDA of INR 8.0 bn.

- Growth Profile: Revenue grew by 7.5% per year from INR 22 bn in FY16 to INR 42 bn in FY25 (Table 1). Further, revenue grew by 11.4% from INR 31.1 bn in 9M FY25 to INR 34.6 bn in 9M FY26. 7year, 5year, and 3year revenue CAGR stood in the range of 7-9%.

- Segment growth Divergence: Personal Care and Beyond category, now comprised 48% of revenue, grew by 10.3% in FY25 outperforming Oral Care growth of 5.6%.

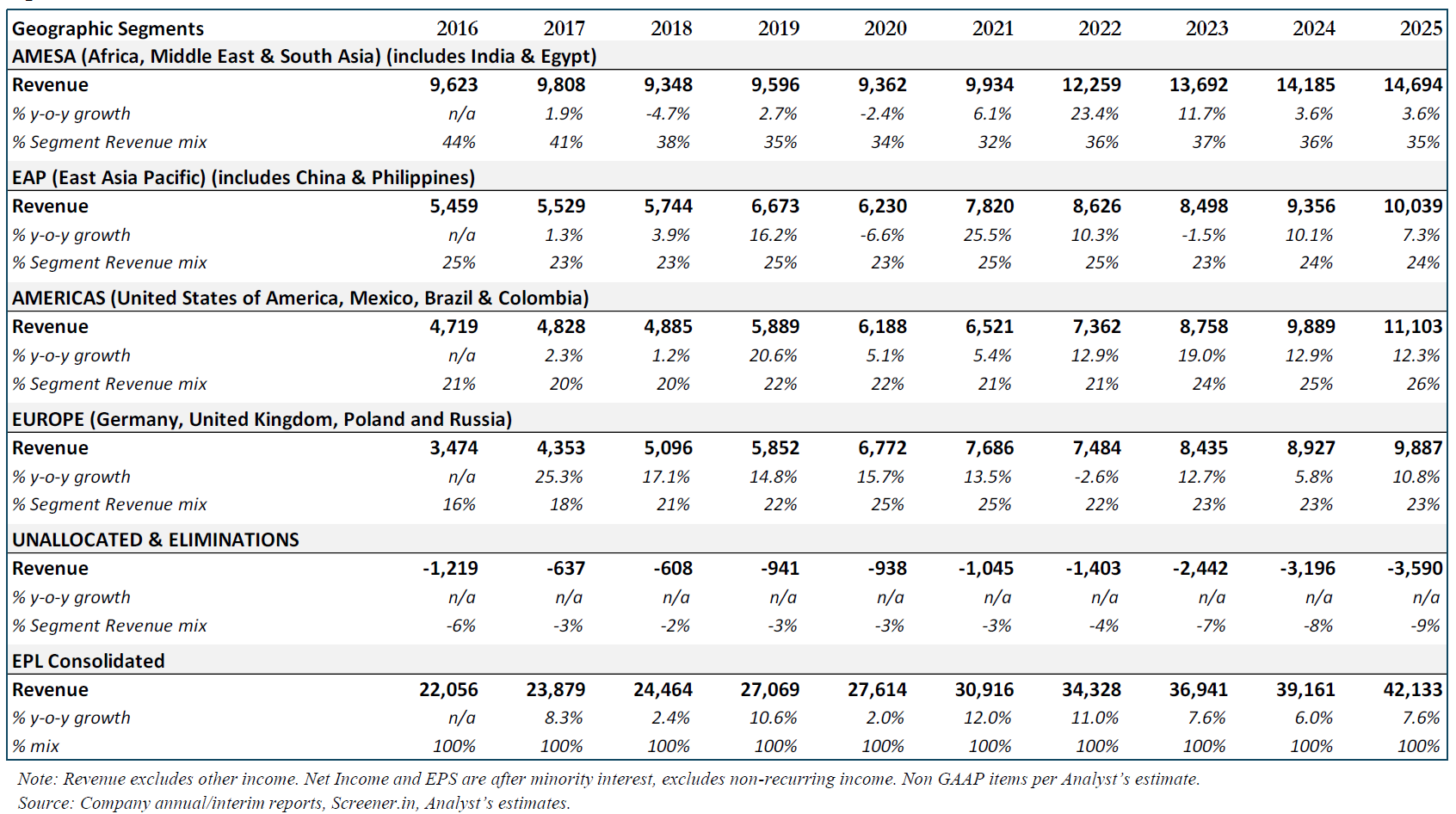

- Geographic Revenue: EPL reported revenue under four segments in FY2025 – AMESA (35% of revenue), EAP (24%), AMERICAS (26%), and Europe (23%) (Table 2).

-

- The long-term revenue growth of EPL has been led by the Americas and Europe, which grew their collective revenue share from 37% in FY16 to ~50% in FY25.

- While AMESA remains the largest single region, its dominance is steadily eroding. Its revenue contribution has dropped from 44% to 35% over the last decade as the business successfully diversified into Western markets.

-

- Customer Concentration: A sizable portion of revenue is concentrated within top accounts, implying maintaining wallet share and diversifying within segments as critical risk factors.

- Long-term relationship with Clients: ~50% of total revenue is derived from contracted customers under long-term repeat supply relationships.

- Trajectory and Drivers of Margin Expansion: EBITDA grew by 8.4% per year from INR 4 bn in FY16 to INR 8 bn in FY25. EBITDA margin expanded from 18.3% to 19.8% during the same period. EBITDA margin further improved to 20.5% for 9M FY25. EBITDA margin expansion in recent years reflect cost saving initiatives, and favorable product mix, and improved performance in Europe and the Americas.

- Product Mix Shift: The category mix continued to shift favorably i.e. towards Personal Care and Beyond, which now accounts for 48% of the revenue. Personal Care and Beyond category has higher EBITDA margin and grew by 10.3%, compared to 5.6% growth of Oral Care in FY25.

- Cost Structure: The overall cost structure includes raw materials ~40% of revenue, employee benefit expense ~20% of revenue, and other administrative expense ~20% of revenue.

- Margin Risk and Volatility: EBITDA margins is highly susceptible to change in raw material prices such as polymers which are influenced by crude oil and global supply demand factors. Any supply disruption or pricing surge to affect profitability. Volatility and shortage in input material prices, inflationary environment, supply chain disruption and wage inflation & absenteeism along with continued global Covid19 pandemic situation impacted the profit margin of the Company in FY22. EBITDA margin had declined from 19.8% in FY21 to 16.8% in FY22 and to 15.6% in FY23 (Table 1)

- Cash Flow Quality and Trajectory: Operating cash flow generation is structurally healthy but cyclical in nature. Cumulative cash flow from operation (CFO) has averaged ~80-85% of EBITDA over the last 5 years, indicating earnings are largely cash-backed. The sharp dip in FY22 (54%) reflects working-capital pressure and cost shocks.

- CFO Conversion Trend: Cash conversion shows resilience across cycles, but not linearity. CFO conversion rebounded strongly post-FY22, crossing 100% in FY23 and remained elevated in FY25 (95%). This indicates normalization of working capital and improved cash discipline (Table 3)

- Capital Intensity: Capex intensity is structurally high reflecting the capital-intensive nature of the industry. Capex averaged ~45% of EBITDA over the last 5 years on a cumulative basis.

- FCF Volatility: Free cash flow is volatile, driven by capex cycles. FCF conversion has ranged widely (6% to 62% of EBITDA), with troughs in FY19 and FY22 coinciding with heavy capex. Despite volatility, the 5-year average FCF conversion seems to be stabilizing at ~40%, suggesting EPL is a steady but not a very high free-cash compounding business.

- Recent Performance: FY25 represents a strong cash recovery year. FY25 FCF of INR 4.3bn (52% of EBITDA) reflects a favorable mix of strong CFO and moderated capex.

- Return on Invested Capital (ROIC): Mid-teen through cycle. ROIC largely stable at ~15% pre-FY21, dipping to 11–13% in FY22 – FY23, and recovering to 16% in FY25.

- Adjusted Return on Equity: Adjusted ROE followed a similar trajectory. Average 18% pre-FY21, declining to ~14%in FY22 – FY23, and recovering to 18% in FY25.

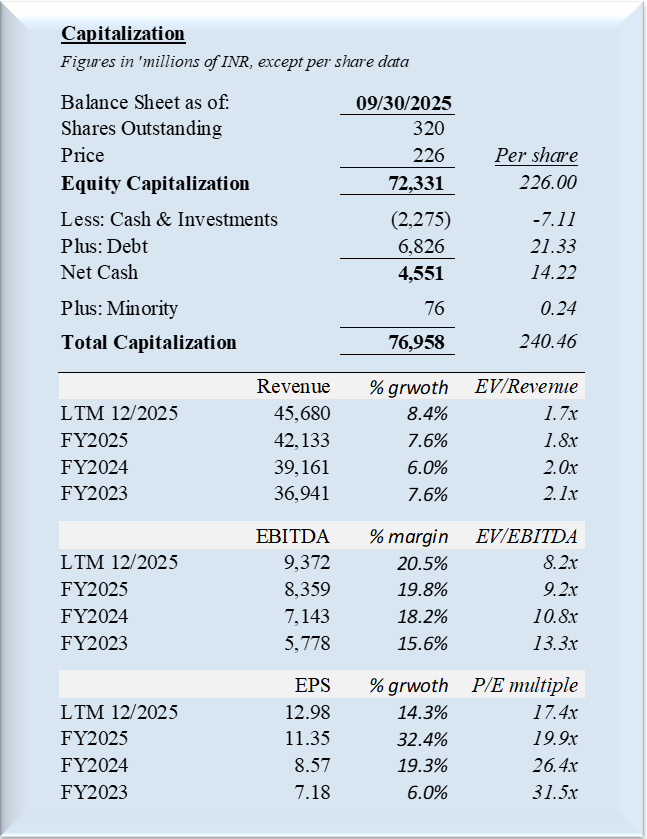

- Cash & Cash Equivalent: INR 2.3 bn or INR 7 per share (as of 09/2025).

- Debt: INR 6.8 bn or INR 21 per share. Total debt to LTM EBITDA ~0.7x (No significant debt). Debt to EBITDA ratio to improve post its merger with Indovida.

- Paid INR 5 per share in dividend. Implied dividend yield 2.2%.

- Geographical Expansion: EPL is Scaling manufacturing footprint. The Brazil facility is fully operational. A new greenfield project in Thailand is under development. The Company has historically serviced parts of the region through exports from China and has established customer relationships and a visible order pipeline. In parallel, EPL is increasing exports from its India and China operations to serve global customers more efficiently.

- Portfolio Mix Upgrade: Increasingly focus on high margin Beauty & Cosmetics and Pharma.

- Wallet Share Expansion: Continued efforts to increase wallet share expansion with existing customers through expanding product offerings and cross-selling across regions.

- Operational Efficiency and Cost Optimization: EPL continues to focus on operational efficiencies through automation, process optimization, and cost-control initiatives across its manufacturing footprint.

- Sustainability: Per EPL, their ‘Neo Seam’ technology, which eliminates the side seam impact, has entered the market and is gaining traction across regions.

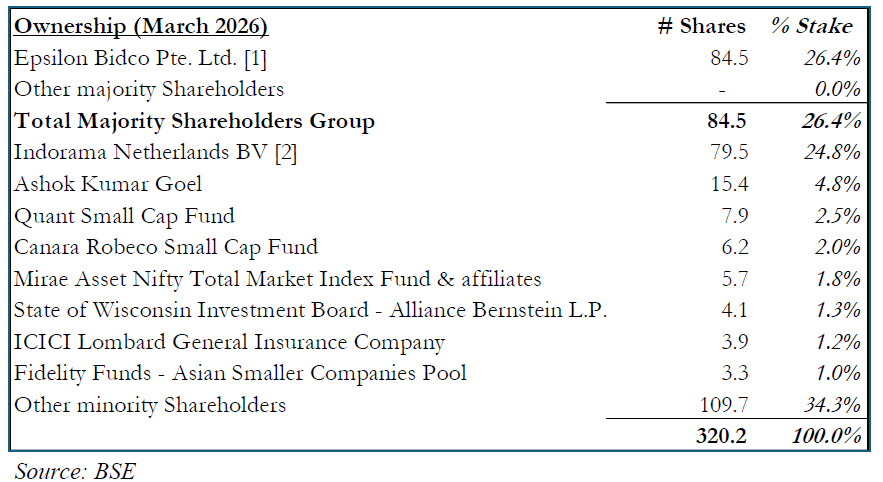

- Key Shareholders: Epsilon Bidco, part of the Blackstone group and the majority shareholder, owns 26% stake in EPL. Indorama Netherlands BV is the largest minority shareholder with 24.8% stake. Ashok Kumar Goel, Quant Small Cap Fund, Canara Robeco Small Cap Fund, and Alliance Bernstein L.P. are the other major minority shareholders of EPL.

- Ownership Change:

-

- On March 29, 2026, the board of EPL approved the merger of Indovida India Private Limited into EPL through an all-share transaction. Indovida is a wholly owned subsidiary of Indorama Ventures. Under the approved swap ratio, Indorama will receive 286 EPL shares for every 10,000 Indovida shares, resulting in a 51.8% ownership in EPL post-merger. Blackstone’s stake is expected to decline from ~26% (Mar 2026) to ~16.6% post-merger. The transaction is subject to regulatory and shareholder approvals and is expected to close by end of FY2027.

- On February 24, 2025, Blackstone had announced entering into a definitive agreement with Indorama Netherlands, B.V., a group entity of Indorama Ventures to sell a minority stake in EPL. INBV acquired a minority stake of ~24.9% of EPL from Blackstone at a purchase price of INR 240 per share.

-

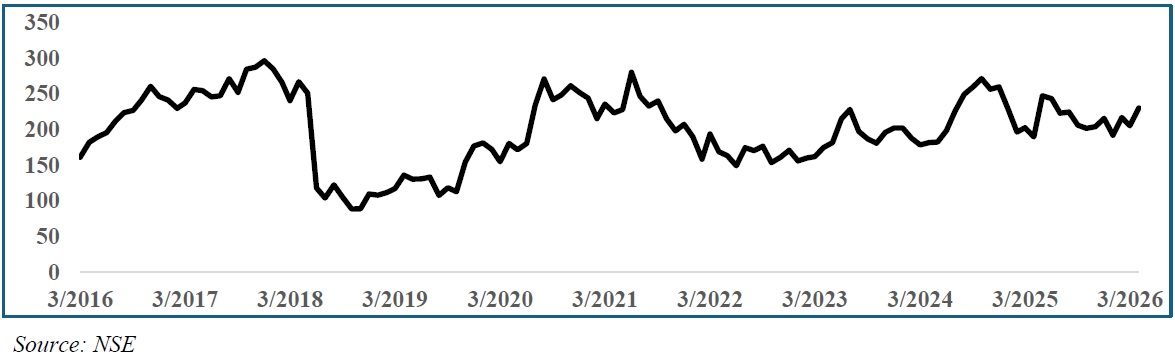

- At a share price of INR 226 (as of April 30, 2026), EPL has a market capitalization of ~INR 72 bn and an enterprise value of around INR 77 bn. Based on LTM financials as of Q3 FY26, EPL trades at 8.2x LTM EBITDA of ~INR 9 bn, and 17x LTM earnings of ~INR 13 per share.

- At current levels, EPL trades below both recent private-market transaction benchmarks and its own long-term trading valuation averages.

-

- The recently announced merger of Individa and EPL implies a pro forma valuation of ~10x EV/EBITDA for the combined entity.

- Blackstone acquired a majority stake in EPL in April 2019 at an implied valuation of ~9x EV/EBITDA.

- Indorama Netherlands B.V. acquired a significant minority stake in February 2025 at an implied valuation of ~10x EV/EBITDA.

- EPL’s 5-year // 10-year median EV/EBITDA multiples stand at 10x, and P/E multiple stand at 26x // 24x and (per Screener.in as of April 27, 2026).

-

- This valuation discount persists despite a larger revenue base, higher absolute EBITDA, improved geographic diversification, and a recovery in margins and cash generation following the FY22–FY23 cost shock. Over time, EPL has demonstrated the ability to protect earnings, restore margins, and convert profits into cash across periods of input-cost volatility and operational disruption.

- From a capital allocation perspective, EPL offers a combination of steady earnings growth, resilient operating cash flows, and reinvestment capability. The current valuation provides a margin of safety relative to the company’s historical trading range.

DISCLOSURES AND DISCLAIMERS

- Analyst’s Position Disclosure: Anand Rawani holds shares of EPL. Date of last transaction: April 9, 2025. Transaction type: Buy. Transaction price: INR 181.57 per share.

- Analyst’s Remarks: Stock recommendations are suitable only for investors with long term investment horizon, typically 5 years and above.

Disclosures and disclaimers: Anand Rawani is registered with Securities and Exchange Board of India (SEBI) as a Part-time Research Analyst (RA) with registration number INH000022039. The RA is also enlisted with Bombay Stock Exchange with BSE enlistment number 6606. The RA publishes equity research and analysis on MoatLane.com, offering stock research reports, newsletters, and model portfolios. MoatLane.com is wholly owned by the RA. All research is based on publicly available information, third-party data, and proprietary analysis. The RA does not provide portfolio management, investment advisory, merchant banking, brokerage, or distribution services. Other business activity: Anand Rawani is employed as Senior Analyst with Horizon Market Research Private Limited, a subsidiary of Teton Advisors, Inc. Teton Advisors, LLC and Keeley-Teton Advisors, LLC are wholly owned subsidiaries of Teton Advisors, Inc. In this role, he is responsible for leading the firm’s sustainability initiatives and risk management functions. He also serves as Director at VernoHR Tech Private Limited, providing oversight and advisory support on finance and accounting matters. He owns a 75% stake in VernoHR Tech Private Limited and the remaining 25% is owned by his family members. Disciplinary history: No disciplinary action has been taken by SEBI or any other regulatory authority against the RA as of the date of this document. Terms and conditions of research services: Research is offered to subscribers and clients on a paid basis, with fees disclosed in advance. Reports are for informational and educational purposes only; they are not investment advice or solicitation. Clients are encouraged to seek independent financial advice before acting on research opinions. No assurance or guarantee of investment returns is provided. Investor shall take note that investment in stocks or other securities is always subject to market risk. Past performance is never a guarantee of same future results. The RA will not provide any execution or distribution services. Use of artificial intelligence: The use of artificial intelligence (AI) tools, such as ChatGPT, Copilot, and Perplexity, is limited to supporting certain operational tasks, including drafting, rewriting, summarizing content, and enhancing communication. These tools are not used for investment idea generation, stock selection, or portfolio decision-making. All research, analysis, and recommendations are based on independent judgment, fundamental research, and analyst expertise. Ownership and material conflicts of interest: RA, associates, or relatives may have financial interests in companies covered in research reports. Any such interest will be disclosed in the respective research reports or public appearances. The RA, associates, or relatives may hold 1% or more beneficial ownership of securities of subject companies. Such holdings will be disclosed in the relevant reports. Any material conflict of interest at the time of research publication or appearance will be disclosed. Compensation disclosures for research reports: RA or associates have not received compensation from a subject company in the past 12 months. RA or associates have not managed or co-managed public offerings of securities for subject companies in the past 12 months. RA or associates have not received compensation for investment banking, merchant banking, or brokerage services from subject companies. RA or associates have not received compensation for other products or services from subject companies. RA or associates have not received third-party compensation or benefits in connection with research. Compensation disclosures for public appearances: RA or associates have not received compensation from subject companies in the past 12 months. The subject company is or was not a client of the RA or associates during the preceding 12 months. Other disclosures: RA have not served as an officer, director, or employee of a subject company. RA or associates have not engaged in market-making activity for a subject company. Standard warning: Investment in securities market are subject to market risks. Read all the related documents carefully before investing. Disclaimer: Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors. Other disclaimers: The research services are independently offered by Anand Rawani in his capacity as a SEBI-registered Part-time RA (Registration No. INH000022039). They are not affiliated, associated, or endorsed by Teton Advisors, Inc., its affiliates, Keeley Teton Advisors, LLC, Teton Advisors, LLC, Horizon Market Research Private Limited, or VernoHR Tech Private Limited. The information and opinions in this research are based on sources believed to be reliable but are not guaranteed for accuracy or completeness. This material is for informational purposes only and does not constitute investment advice, solicitation, or recommendations. The RA and associates accept no liability for losses from use of this content. Investors should conduct their own research and seek professional advice before making investment decisions.